Global share markets fell again over the last week as bond yields rose further (with Fed Chair Powell offering no objection to rising bond yields in a Q&A session) putting more pressure on share market valuations. September lived up to its reputation as being a bad month for shares with US shares down around 4.6% and global shares down around 3.7%. Australian shares fell but only by around 0.2% for the week with falls led by IT, materials and discretionary stocks, leaving it down around 3.4% for September. Bond yields rose further, with the Australian 10-year yield rising to its highest since 2011. Oil and metal prices rose but iron ore prices fell. The $A rose slightly, despite a further in the $US.

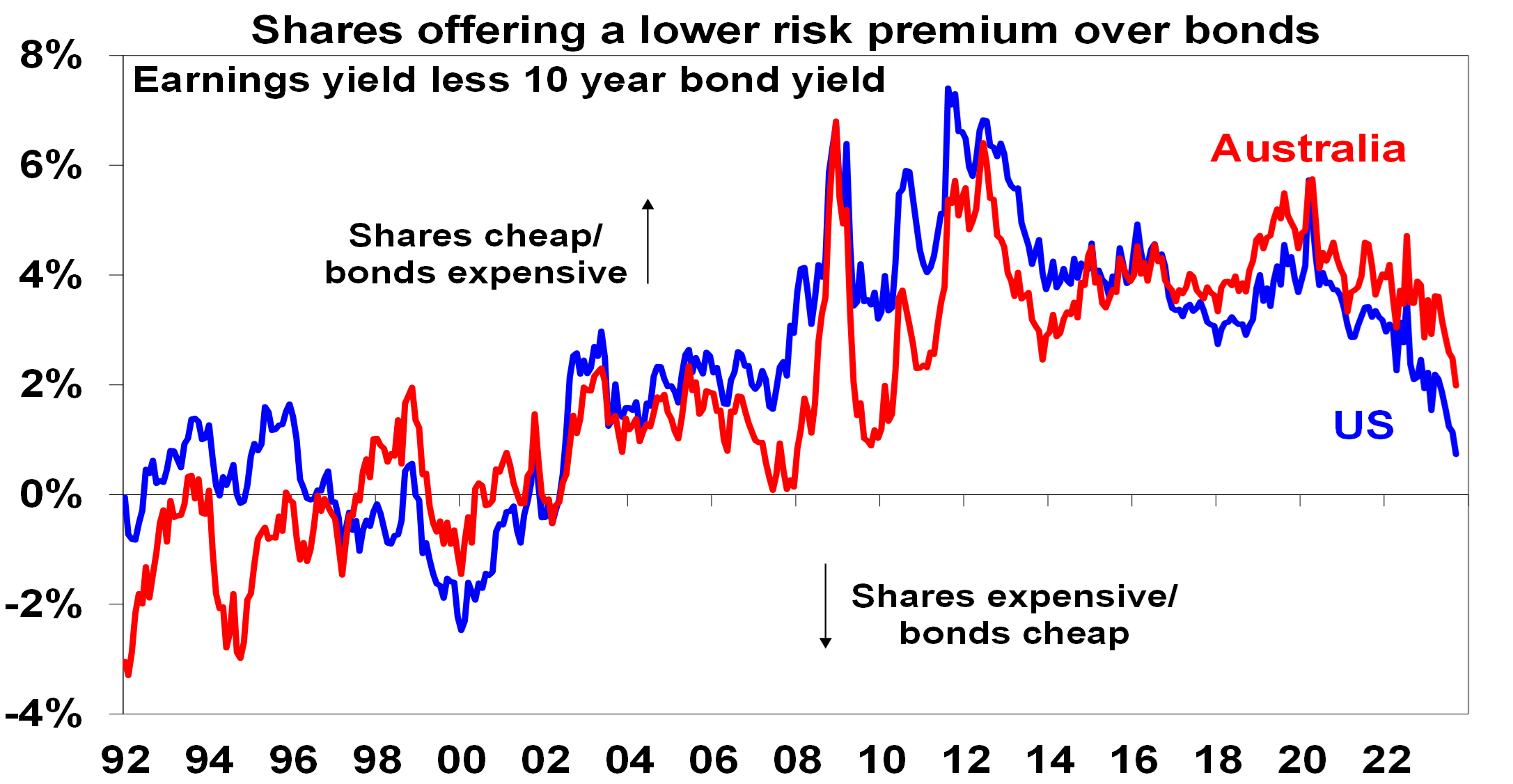

From their July highs US shares have had a fall of 7% and global and Australian shares have had falls of 6%. Shares have become oversold and due for a bounce, but the risk of a further correction beyond any near-term bounce is high. The ongoing rise in bond yields on the back of central bank warnings of higher rates for longer have pushed the risk premium that the key direction setting US share market offers over bonds to its lowest in over 20 years. (See the next chart.) Meanwhile, the risk of recession remains high, the continuing rise in oil prices is adding to the risk recession, uncertainty remains high around the Chinese economy, a US Government shutdown is increasing uncertainty about the US economy & fiscal policy and the period into mid-October is often seasonally weak for shares. All of which leaves shares vulnerable at a time when US valuations are looking very stretched and will become even more so if bond yields keep rising. While valuations for the Australian share market are more attractive – see the next chart – it would likely follow any further correction in US shares in the short term. Our 12-month view on shares remains positive though as inflation is likely to continue to trend down taking pressure off central banks and any recession is likely to be mild.

Source: Bloomberg, AMP

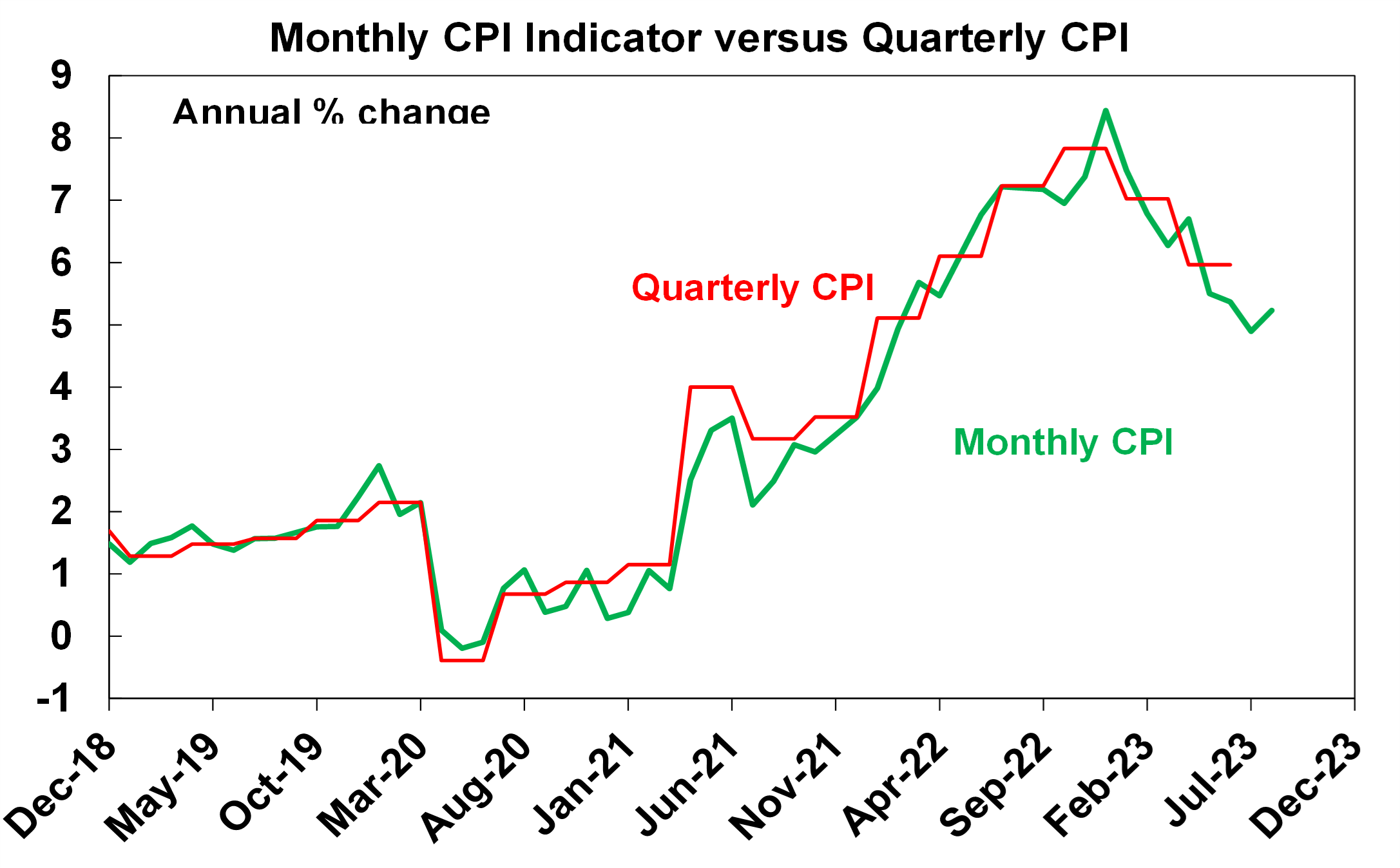

After falling more than expected in July to 4.9%yoy, the Australian Monthly Inflation Indicator rose in line with expectations in August to 5.2%. This is similar to the experience seen in several other countries.

Source: ABS, AMP

The trend remains down in Australian inflation, but inflation is still too high. The good news is that: all of the rebound in inflation in August was due to a 9.1% rise in auto fuel prices which added 0.3% to inflation; underlying measures of inflation were flat or down with the trimmed mean inflation rate unchanged at 5.6%yoy and the CPI excluding volatile items and travel falling to 5.5%yoy; energy subsidies are continuing to take the edge off electricity price rises (which fell in August); and numerous items are showing a slowdown in annual inflation (including food, housing, furnishings and household equipment and recreation & culture with falling travel costs) or low inflation (notably clothing and communications). The bad news though is that: fuel prices likely have more upside; several items are continuing to see an acceleration in inflation (notably rents, education and insurance); and services inflation remains sticky even though goods price inflation is cooling.

Source: ABS, AMP

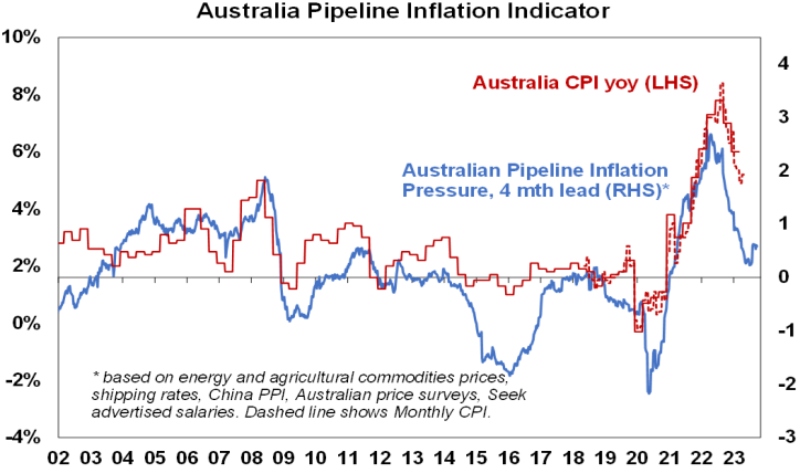

While our Australian Pipeline Inflation Indicator has picked up it continues to point to a further sharp fall in inflation ahead.

Source: Bloomberg, ABS, AMP

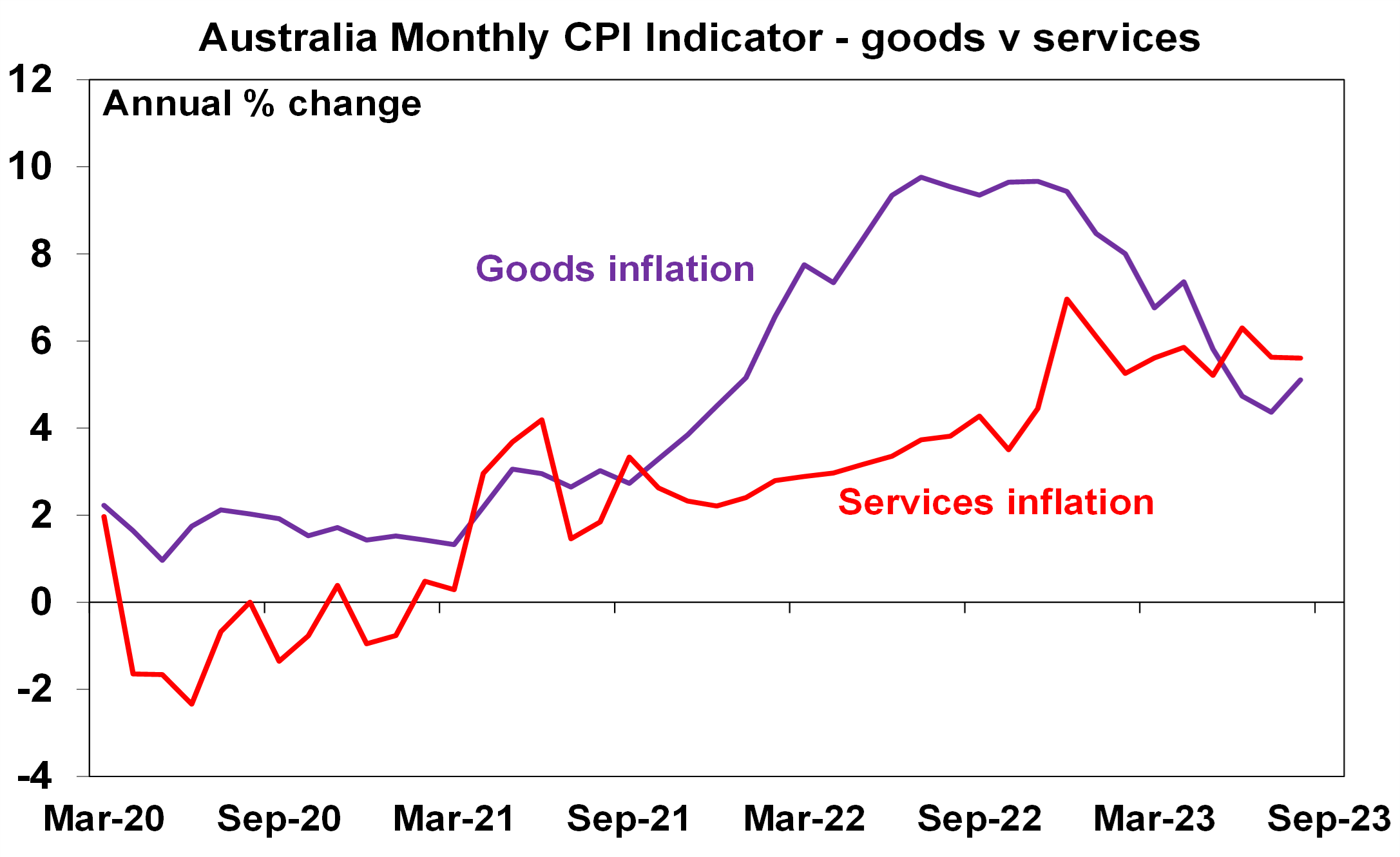

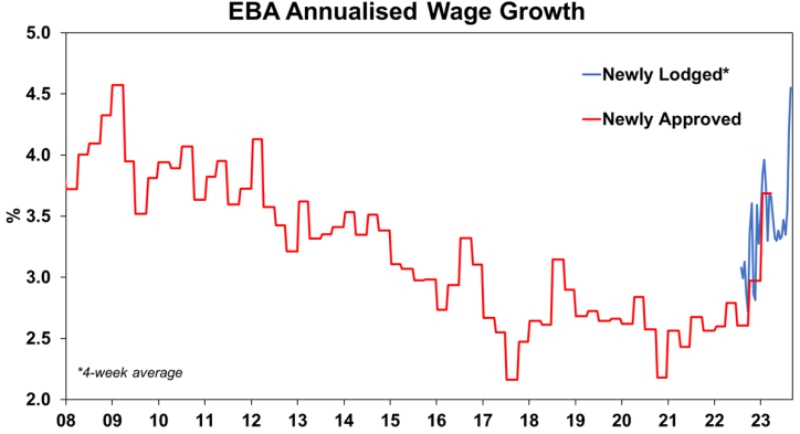

Services inflation in Australia is likely to follow goods price inflation down as the economy continues to slow – however the risk around this is high due to a rising risk that wages growth may be moving above 4%. This is highlighted by newly lodged Enterprise Bargaining Agreements showing an acceleration in wages growth to 4.7%pa and advertised salaries on Seek now running up 5.1%yoy. This all follows the Fair Work Commission’s granting of an 8.6% increase in minimum wages and 5.75% increase in award wages which are likely to have had an influencing effect on other wage negotiations. An acceleration in wages growth much above 4% would be seen by the RBA as inconsistent with its 2-3% inflation target and run the risk of entrenching inflation at high levels. The surge in petrol prices could also boost inflation expectations but given the pressure household budgets are under it will more likely act as a tax on spending than as a boost to underlying inflation.

Source: Fair Work Commission

The RBA is expected to leave rates on hold at 4.1% on Tuesday. Since the last RBA board meeting the combination of softening full time jobs growth and a further fall in job vacancies, real retail sales continuing to fall and the underlying trend in inflation remaining down all against the background of tight monetary policy are consistent with the RBA remaining in “wait and see mode” and therefore leaving interest rates on hold for the fourth month in a row. Our assessment remains that the RBA has done more than enough to control inflation and that rates have peaked ahead of rate cuts starting around June next year.

However, the RBA is likely to reiterate its tightening bias “that some further tightening of monetary policy may be required” and the risk of another hike by year end has gone up to around 40% in our view with still sticky services inflation, increasing upside risks to wages growth, poor productivity and upside risks to inflation expectations posed by higher petrol prices. Against this though another rate hike would be very high risk as economic data is already slowing and we remain of the view that the risk of a recession is already around 50%. If new Governor Bullock is to raise rates again though she is likely to wait to see the September quarterly CPI and updated RBA forecasts which will both be available by the November meeting and possibly September quarter wages data (due in mid November) which could take us to the December meeting. The money market is attaching a zero probability to a hike on Tuesday (which seems way too low), but 94% chance of a 0.25% hike by May next year.

The Australian Government’s Employment White Paper makes great sense as we should be working to lower structural unemployment – but the risk is that its offset by labour market re-regulation. The White Paper said all the right things: we need to focus more on labour market underutilisation and not just on a narrow definition of unemployment; we need to draw on the 2.8 million Australian’s who are unemployed, underemployed or who want to work but face various barriers; we need to lower the level of structural labour underutilisation (ie a broader concept of NAIRU to include the unemployed and underemployed) below which inflation starts to rise; and this is not something the RBA can do but it is something the Government can do by removing skill mismatches and reducing barriers to work. And so, its good news to see the Government starting to focus on this more systematically. Of course its not going to be easy as it will take time, many of the proposed policies referred to in the White Paper are similar to initiatives of previous governments, trying to accurately anticipate future workforce skill requirements and eliminate skill mismatches will be hard, and the Government’s own moves to re-regulate the labour market and reduce job market flexibility risk working in the opposite direction by pushing structural labour underutilisation up.

US political dramas – notably Presidential elections, mid term elections, debt ceiling dramas and Federal government shutdowns – are a tedious fact of life that invariably impact investment markets (albeit usually by much less than feared). Once one ends, we then move on to the next one. Right now, it’s a Government shutdown. Here is a brief summary.

- Congress needed to pass a new budget or a continuing funding resolution by 1 October, the start of the new fiscal year, to avoid a shutdown.

- What is relevant is the chamber in Congress that’s controlled by the opposition Republicans and right now that’s the House. So the Democrat controlled Senate can pass a stop gap funding measure but unless House Speaker McCarthy allows a vote on it (which would likely pass) then its academic.

- And right now he is under high pressure (at risk of losing his job) from conservative Republican’s to hold firm in demanding reduced spending in the face of very high debt levels and a rising budget deficit. So he may not want to rush into it.

- And President Biden may benefit politically from standing firm against spending cuts.

- Historically both sides of politics are usually seen to blame for shutdowns, but more so Republicans so they usually compromise eventually.

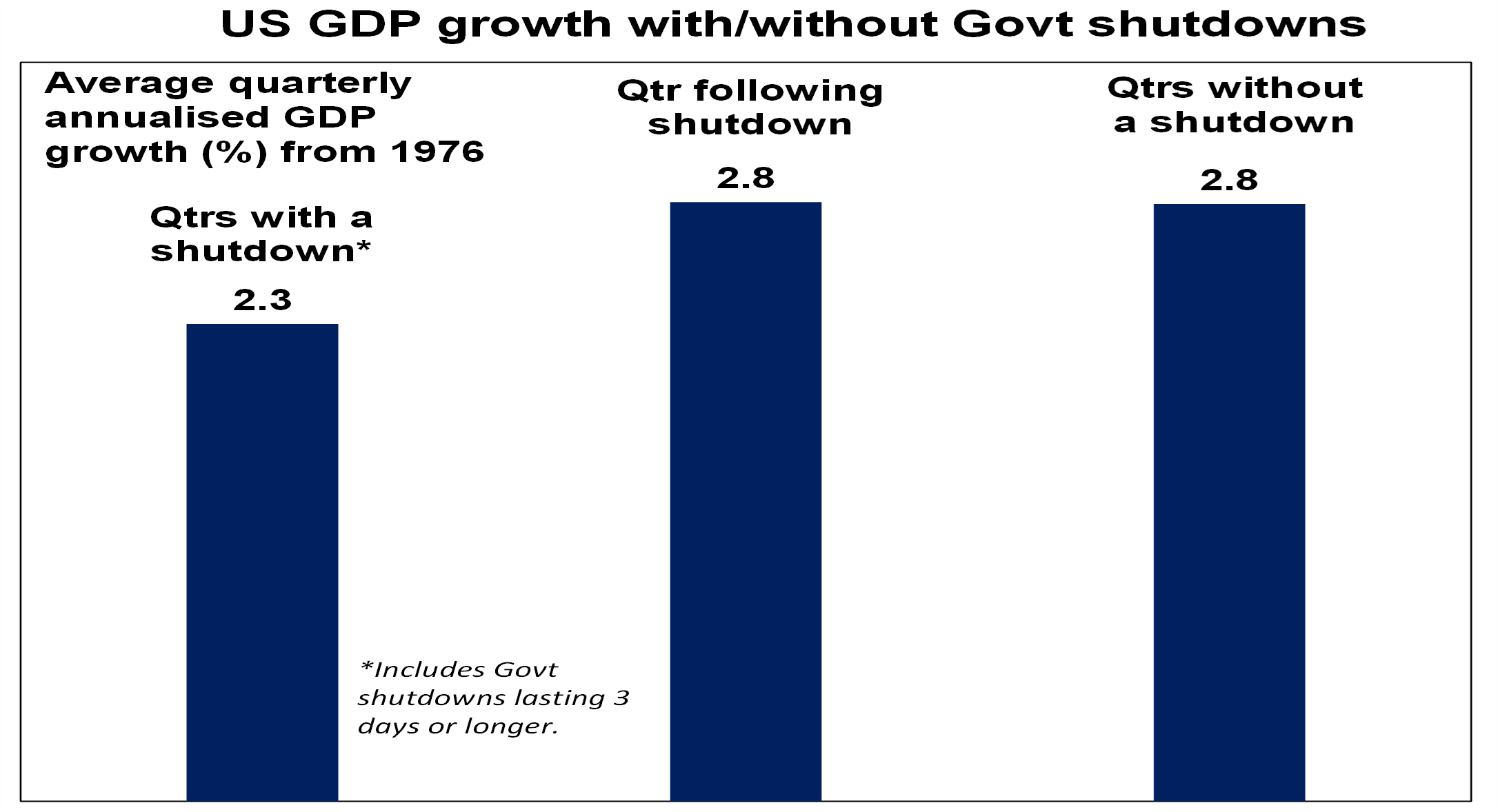

- Since 1976 the US has had 21 government shutdowns with an average duration of around 8 days ranging from 1 day up to 35 days (which was in 2018-19).

- Usually, they are only a partial shutdown and their economic impact tends to be minor with a catch up including in public servants pay after they end.

- Since 1976 quarters with shutdowns of 3 business days or more averaged GDP growth of 2.3% annualised versus quarters with no shutdown having 2.8% annualised growth, which means an average difference of just 0.14% at a quarterly rate. A rough rule of thumb is that each week in shutdown cuts 0.1% from GDP.

- When economic conditions are already uncertain like at present a shutdown could add to share market volatility.

- A particular risk at present would be if Moody’s (the remaining top 3 ratings agency to still have US debt rated at AAA) downgrades US Government debt on the grounds that a shutdown highlights weakness in US institutions and governance, as its already threatened to do.

- One aspect is that through a shutdown US economic statistics won’t be published – so US economists can have a break and the public can have a break from hearing from them! Maybe we should try that in Australia!

Source: Bloomberg, AMP

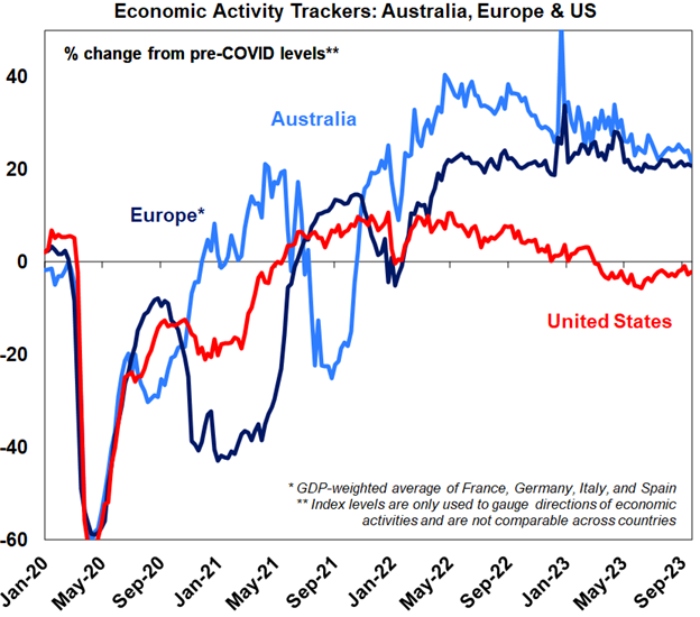

Economic activity trackers

Our Economic Activity Trackers are still not providing any decisive indication of recession or a growth rebound.

Levels are not really comparable across countries. Based on weekly data for eg job ads, restaurant bookings, confidence, credit & debit card transactions and hotel bookings. Source: AMP

Major global economic events and implications

US economic data was mostly soft. Home prices rose again in July, but a continuing plunge in mortgage applications on the back of still rising 30-year mortgage rates point to housing sector weakness ahead. Consistent with this new and pending home sales fell sharply in August. Consumer confidence fell partly reflecting the rebound in gasoline prices and perceptions of whether jobs are easy to get remained well down from its highs. Capital goods orders excluding volatile items rose slightly but look flat since mid-last year.

Source: Macrobond, AMP

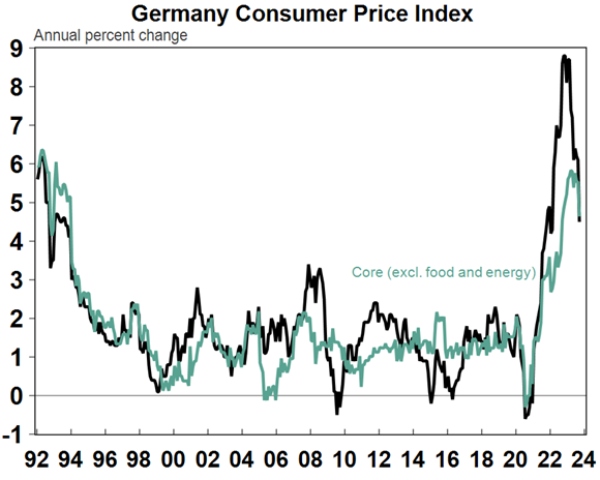

German inflation fell more than expected to 4.5%yoy in September and Eurozone economic sentiment fell but by less than expected.

Source: Macrobond, AMP

Japan’s jobless rate was flat at 2.7% in August and retail sales growth remained solid at 7%yoy, but industrial production remained weak at -3.8%yoy highlighting a dichotomy between solid domestic demand but weak global demand. September inflation in Tokyo slowed with core (ex food & energy) inflation falling to 2.4%yoy.

Australian economic events and implications

Australian economic data was soft. Retail sales rose 0.2% in August and are up just 1.5% on a year ago. This was slightly less than most economists expected and is actually pretty soft given a boost to clothing and accessory sales from warmer than normal weather, a boost to fan gear demand and spending in cafes etc from the 2023 FIFA Women’s’ World Cup, Afterpay Day promotions, the fastest population growth since the 1950s and still high inflation. The 0.2% rise in August followed a 0.5% rise in July but a 0.8% fall in June and since October/November last year they have been flat in nominal terms. September quarter real retail sales are on track for their fourth quarterly fall in a row highlighting the pressure on households from interest rate hikes and cost of living pressures. In fact, on our estimate real retail sales per person are down around 4.5% on a year ago.

Source: ABS, AMP

Job vacancies show that the labour market is still tight but its rapidly cooling. The ABS’ survey of job vacancies fell 8.9% over the three months to August, leaving them down for five quarters in a row by 18%. The proportion of businesses reporting vacancies is also falling. This has taken the ratio of job vacancies to unemployed down from 1 in July last year (ie for every unemployed person there was one job vacancy) to now 0.7. While vacancies are still high, they are falling quickly and warn that the labour market is cooling rapidly. Its quite likely that the surge in population growth is accentuating this along with slowing demand growth in the economy but it all points to a softer labour market and higher unemployment ahead.

Source: ABS, AMP

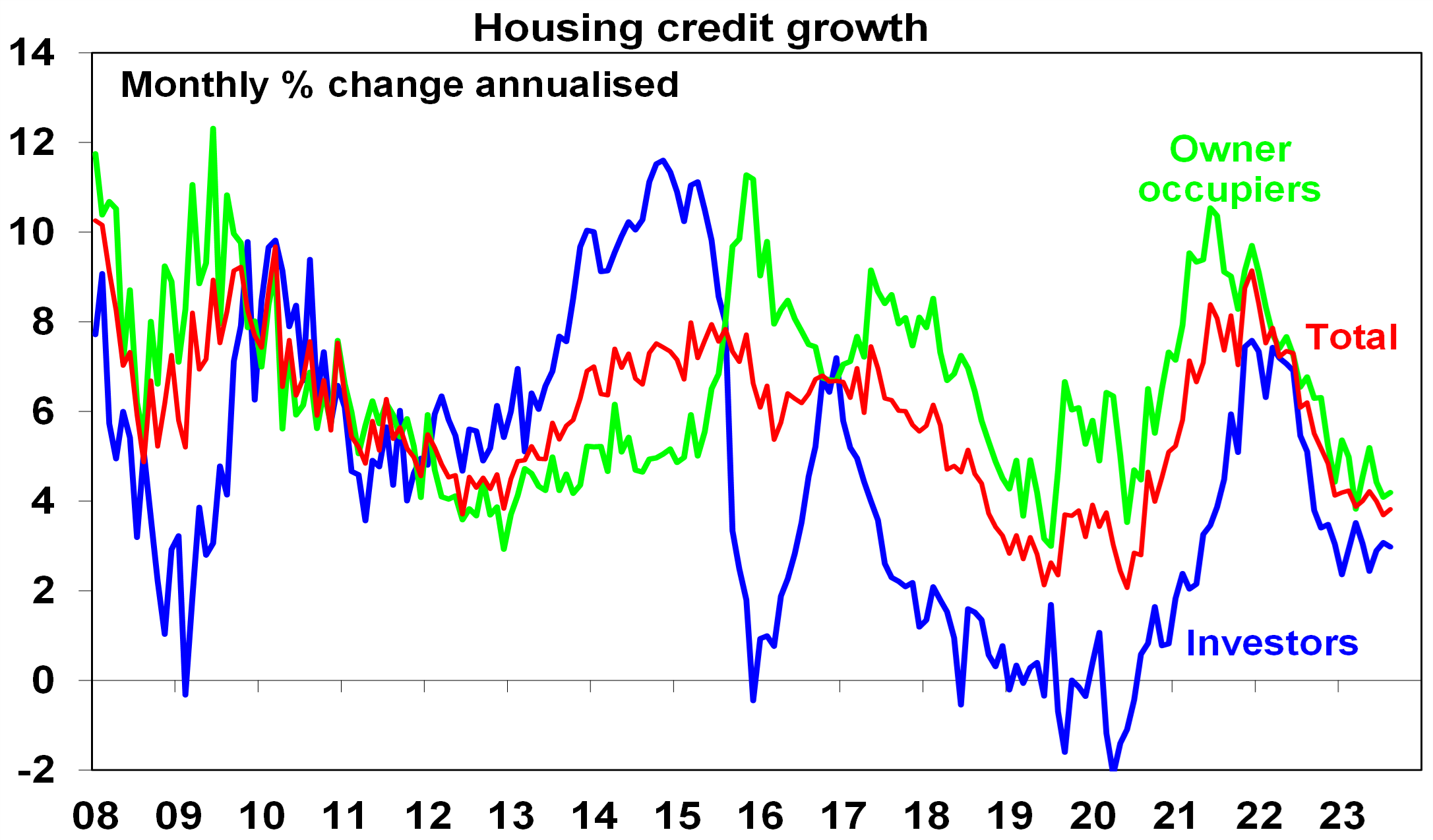

Private sector credit data showed housing credit growth remains modest. Past home price rebounds would have normally seen a bit more of a pick up by now but this one has come on relatively low volumes and existing borrowers trying to pay down debt more rapidly.

Source: RBA, AMP

What to watch over the next week?

In the US, the focus is expected to be on September jobs data to be released Friday (unless it’s delayed by a Government shutdown). Payroll growth is expected to slow to 170,000, with unemployment falling back slightly to 3.7% (from 3.8%) and wages growth of 0.3%mom and unchanged at 4.3%yoy. September ISM business conditions PMIs are expected to show a slight improvement in manufacturing to around 47.8% (Monday) but a slight fall in services (Wednesday). Job openings data for August (Tuesday) are expected to show a further fall.

Eurozone jobs data for August (Monday) is expected to show unemployment unchanged at 6.4%.

Japan’s third quarter Tankan business conditions survey (Monday) is expected to show continued solid conditions particularly for services.

The Reserve Bank of New Zealand (Wednesday) is expected to leave its cash rate on hold at 5.5%.

In Australia, as noted earlier, the RBA (Tuesday) is expected to leave rates on hold at 4.1% for the fourth month in a row but its likely to retain its tightening bias. On the data front expect CoreLogic data for September to show a 0.9% rise in capital city home prices (Monday), August data to show a 5% rise in building approvals after two months of big falls and a 0.3% fall in housing finance (Tuesday) and the trade surplus to rebound to $9.3bn (Thursday). The RBA will release its bi-annual Financial Stability Review on Friday which will be watched for its latest assessment as to how household finances are weathering the rise in interest rates.

Outlook for investment markets

The next 12 months are likely to see a further easing in inflation pressure and central banks moving to get off the brakes. This should make for reasonable share market returns, provided any recession is mild. But for the near term shares are at high risk of a further correction given high recession and earnings risks, the risk of higher for longer rates from central banks, rising bond yields which have led to poor valuations and poor seasonality into October.

Bonds are likely to provide returns above running yields, as growth and inflation slow and central banks become dovish but given the recent rebound in yields this may be delayed a few months.

Unlisted commercial property and infrastructure are expected to see soft returns, reflecting the lagged impact of the rise in bond yields on valuations. Commercial property returns are likely to be negative as “work from home” continues to hit space demand as leases expire.

With an increasing supply shortfall, our base case remains that home prices have bottomed with more gains likely next year as the RBA starts to cut rates. However, uncertainty around this is high given the lagged impact of interest rate hikes and the likelihood of higher unemployment.

Cash and bank deposits are expected to provide returns of around 4-5%, reflecting the back up in interest rates.

The $A is at risk of more downside in the short term on the back of a less hawkish RBA and weak growth in China, but a rising trend is likely over the next 12 months, reflecting a downtrend in the overvalued $US and the Fed moving to cut rates.

What you need to know

While every care has been taken in the preparation of this article, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided and must not be provided to any other person or entity without the express written consent AMP. This article is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.

The information on this page was current on the date the page was published. For up-to-date information, we refer you to the relevant product disclosure statement, target market determination and product updates available at amp.com.au.